The United Kingdom is once again at a pivotal moment in its monetary policy cycle. After months of speculation and mounting economic headwinds, on 6 August 2025 the Monetary Policy Committee (MPC) voted to lower the Bank of England base rate from 4.25 % to 4.00 %, by a tight 5–4 margin.

Then in September, the MPC opted to hold the rate at 4.00 %, with a 7–2 vote in favour of maintaining rather than cutting further.

This blog explores why the MPC made that call, how the adjustment filters through to mortgages, savings, pensions and business, what to watch next, and how households and investors can respond.

How Often Does the Monetary Policy Committee (MPC) Change the Base Rate?

The Monetary Policy Committee (MPC)—a group of nine experts appointed by the Bank of England—meets eight times each year (roughly every six weeks). During these sessions, the committee votes on whether to raise, cut, or maintain the base rate after analysing the latest economic and global data.

Each decision is made in response to a range of key indicators, including:

- Inflation trends (currently 3.8%)

- GDP growth and employment levels

- Energy prices and global trade risks

- Household borrowing and consumer spending

The MPC operates transparently, individual votes are published in the meeting minutes. Occasionally, unscheduled or emergency meetings occur if economic shocks demand immediate action (though this remains rare).

For 2025, the key MPC meeting dates include:

- 7 August 2025: rate cut from 4.25% to 4.00%

- 18 September 2025: rate held at 4.00%

- 6 November 2025: next scheduled decision

These predictable review points give banks, investors, and households time to adjust their financial plans and prepare for market movements.

What Is the Current Bank of England Base Rate as?

As of 18 September 2025, the Bank of England Base Rate (also known as the Bank Rate) stands at 4.00%, following a 0.25 percentage-point reduction in August 2025.

This decision reflects the MPC’s consensus that inflation is falling but remains above the 2% target, and that the economy still requires support amid slower growth and a cooling labour market.

At the September meeting, seven members voted to maintain the rate at 4.00%, while two advocated a further cut to 3.75%.

This split vote underlines a cautious but slightly dovish tone, signalling that while the tightening cycle has ended, the Bank isn’t rushing into further cuts until inflation stabilises.

The Bank Rate serves as the benchmark for all UK lending and savings rates. When it moves, it ripples across mortgages, loans, and savings products nationwide.

Why Has It Dropped to 4% in August 2025?

The decision to lower the base rate to 4% was influenced by several key factors:

- Weak growth: The UK economy is showing minimal GDP growth, indicating stagnation.

- Job market slowdown: Unemployment is rising and job vacancies are falling, prompting action.

- Inflation concerns: Inflation is at 3.6% and may peak at 4% in September, though seen as temporary.

- Lower consumer spending: Households are spending less due to high living costs and limited borrowing.

- Global risks: Geopolitical tensions and trade issues are adding pressure to the UK economy

Despite inflation remaining above the 2% target, the overall outlook prompted a cautious cut to boost borrowing, ease financial stress and potentially support business activity and consumer sentiment in the months ahead.

What Does the 4% Base Rate Mean for UK Mortgage Holders?

Mortgage borrowers are among the most directly affected groups. The 4.00% base rate changes how lenders price loans, but its impact differs by mortgage type:

Tracker Mortgages

Tracker mortgages move in line with the Bank Rate plus a fixed margin (for example, +1.25%).

Because of August’s 0.25 pp cut, tracker mortgage holders will see their monthly payments fall—typically effective from 1 September 2025.

Standard Variable Rate (SVR) and Base Mortgage Rate (BMR)

Lenders often adjust SVRs following BoE changes, though not always by the full amount.

Many major lenders have already reduced rates:

- SVR: from 6.99% → ~6.74%

- BMR: from 6.25% → ~6.00%

However, lenders can move at different speeds, depending on their funding costs and risk outlook.

Fixed-Rate Mortgages

Fixed mortgage customers won’t see an immediate change. But if you’re nearing the end of your fixed term, now may be an opportunity to refinance into a lower-rate deal. New fixed offers have already improved compared with earlier in 2025.

Should You Switch Mortgage Types Now?

If your fixed term ends within six months, compare remortgage offers immediately. Conversely, if you expect further rate cuts, remaining on a variable rate could yield additional savings, but only if you can tolerate possible volatility.

Use mortgage calculators or your lender’s online tools to model different scenarios before making any decision.

How Will Savings Be Affected by the Latest Interest Rate Cut?

Savings accounts are likely to feel the negative effects of the 0.25% base rate cut. While reduced rates support borrowers, savers may see a drop in the interest earned on their accounts. Currently, the average savings interest rate is around 3.5%, already 0.42% lower than the previous year.

Key impacts include:

- Lower returns on easy-access savings accounts and cash ISAs

- Reduced appeal of long-term fixed savings products

- Erosion of savings value due to inflation projected at 4% in September

Despite these drops, savers can take proactive steps:

- Shop around for competitive rates

- Consider fixed-term savings to lock in current offers

- Diversify into investment products with higher long-term yields

The real risk is negative real returns, when inflation grows faster than your interest earnings, reducing your money’s value.

Savers should regularly review their accounts and use online tools to estimate returns. In uncertain times, stay flexible with your savings plan and keep easy access to emergency funds.

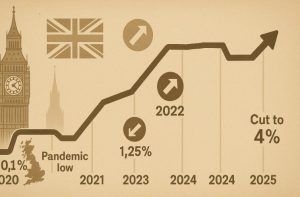

What Is the Historical Trend of the Bank of England Base Rate?

The base rate has experienced dramatic shifts over the past decade. It reached historic lows during the pandemic, standing at 0.1% in March 2020, before steadily climbing due to inflationary pressure. By October 2022, rates began increasing more aggressively, peaking at 4.25% in early 2025.

This change reflects a significant policy shift from stimulating the economy to tackling high inflation. With the recent 0.25% cut, the MPC is attempting to strike a new balance amid evolving economic conditions.

Bank of England Base Rate – Historical Timeline

| Date | Base Rate (%) |

| March 2020 | 0.10 |

| June 2022 | 1.25 |

| October 2022 | 2.25 |

| March 2023 | 4.00 |

| August 2025 | 4.00 (current) |

These changes highlight the dynamic nature of monetary policy, closely tied to inflation, employment and broader economic health.

What Does the Bank of England Base Rate Graph Show About Past Trends?

A visual analysis of the Bank of England’s base rate graph from 2020 to 2025 reveals a sharp incline post-2022, driven by the need to combat rising inflation.

The rate spiked following key political and fiscal events, including the mini-budget of September 2022, which saw market reactions influence lending rates nationwide.

- The graph illustrates volatility from 0.1% in 2020 to over 6% for mortgage products in 2023

- After peaking, the base rate stabilised and is now declining

- Recent declines indicate a shift toward economic support rather than inflation control

This trend suggests a possible downward cycle if economic recovery remains slow. However, any unexpected inflation surge could reverse this path, making future trends unpredictable. The base rate remains a vital indicator of monetary direction in the UK.

Is the 4% Rate Cut Enough to Help the UK Economy Recover?

The 4% rate cut is a strategic step to boost the UK’s sluggish economy, aiming to lower borrowing costs and encourage spending and investment. However, its impact depends on how consumers and businesses respond amid ongoing challenges.

With inflation currently at 3.6% and expected to rise to 4%, real purchasing power may remain limited despite cheaper credit.

Businesses may still hesitate to expand or hire due to rising costs and economic uncertainty. The job market is softening, and wage growth is slowing, both of which signal deeper issues that a rate cut alone may not resolve.

While the cut reflects the Bank of England’s focus on recovery, it also shows a willingness to tolerate higher inflation in the short term. The next Monetary Policy Committee decision in September will be key to shaping the path forward

What Is the Inflation Forecast and Will It Influence Future Rate Changes?

Inflation currently sits at 3.6%, and it is forecast to rise to 4% by September 2025. This is above the Bank of England’s target of 2%, and it adds pressure to the decision-making process regarding interest rates.

Despite this, the MPC believes that the current spike will be temporary, partly driven by food prices and external factors.

Key inflation influences:

- Rising food and energy costs

- Slowing wage growth and weak job market

- Reduced consumer spending

If inflation continues to rise beyond forecasts, future rate cuts may be paused or even reversed. Conversely, if inflation stabilises and growth remains weak, further reductions could be possible.

The Bank of England is carefully monitoring these trends, and each rate decision will reflect a balance between curbing inflation and stimulating economic growth.

What Does the Rate Cut Mean for Pensioners and Retirement Planning?

The base rate cut to 4% has mixed implications for pensioners. While savings returns may diminish, state pension recipients could see benefits due to the inflation-linked triple lock system.

Impact on State Pension

The triple lock ensures that pensions rise each year by the highest of:

- 2.5%

- Average wage growth

- Inflation (measured in September)

If inflation does hit 4% in September, pensioners could see a rise of £9.20 per week for the full new state pension, or £7 for those on the basic state pension in the 2026 financial year.

Impact on Retirement Planning

- Lower savings interest: Retirees relying on interest income will earn less.

- Investment considerations: Some may shift toward diversified or inflation-protected investments.

- Annuities and pension drawdown: Lower rates could impact returns for those buying annuities soon.

Planning is key. Pensioners should review income sources, inflation projections and savings strategies to ensure financial stability through 2025 and beyond. This rate change is a reminder of how sensitive retirement income can be to economic policy decisions.

Conclusion

The Bank of England’s decision to cut the base rate to 4.0% in August 2025 and hold it in September marks a turning point in the UK’s economic cycle. It shows a shift from purely combating inflation to supporting a fragile recovery.

For borrowers, the move offers welcome relief and cheaper credit. For savers and retirees, however, it poses new challenges as real returns dwindle.

The months ahead will be crucial in determining whether the Bank continues to ease policy or holds steady to contain price pressures.

Stay alert to the next MPC announcement on 6 November 2025, as it could set the tone for the UK’s financial outlook into 2026 and beyond.

FAQs About Bank of England Interest Rate Changes

When will the next Bank of England interest rate decision be made?

The next review is set for 18 September 2025. The MPC will review inflation, growth, and labour data before deciding.

Can I lock in a lower mortgage rate now?

Yes, many lenders like Nationwide let you lock in rates up to 6 months in advance online or via a mortgage advisor.

Will the rate cut impact ISA and fixed savings rates?

Yes, rates are expected to drop further, including on easy access accounts, which have already declined over the past year.

Are businesses likely to increase hiring after the rate cut?

Not right away. Hiring depends on inflation, demand, and global conditions despite lower borrowing costs.

What does the Bank of England monetary policy report say about the economy?

The August 2025 report shows weak growth, slowing wages, and inflation expected to peak again before falling later in the year.

Is this the lowest the base rate has been recently?

Yes, 4% is the lowest since March 2023, down from 4.25%, aimed at boosting growth amid uncertainty.

Can I still make overpayments on my mortgage after this rate change?

Yes, overpayments are still allowed and can help reduce your mortgage term and interest paid.

Read Next:

- Thousands of Company Directors Leave UK After Labour’s Tax Changes | Is Britain Losing Its Appeal for Business Owners?

- UK Police Pay Rise 2025 | How Much Is the Confirmed Increase and Updated Pay Scales?

- UK Government to Test Nationwide Armageddon Alert System on Mobile Phones | Why It’s Being Tested?

- Is Martin Lewis Warning NatWest Customers About New Bank Changes?