Getting dismissed from work is stressful, but being sacked for gross misconduct raises even more concerns, particularly about long-term financial security. One of the first questions that often arises is: do you lose your pension if you are sacked for gross misconduct?

The short answer is no, in most cases, your pension stays protected. However, there are some important exceptions, especially for public sector workers, where pension forfeiture rules might apply.

This blog explores how gross misconduct impacts different types of pensions in the UK, what protections exist, when forfeiture might happen, and how you can safeguard your retirement income.

What Does Gross Misconduct Mean in the UK Workplace?

Gross misconduct refers to actions by an employee that are so severe they justify immediate dismissal without notice.

Common examples include theft, fraud, violence, gross negligence, harassment, or serious breaches of health and safety rules. Unlike regular misconduct, which might result in warnings, gross misconduct can lead to instant termination of employment.

Employers must follow fair procedures before dismissing an employee for gross misconduct. This includes investigating the issue, holding a disciplinary hearing, and allowing the employee to respond.

If the employer fails to follow due process, the dismissal could be deemed unfair, opening the door to legal claims, including claims for lost pension contributions.

Knowing what counts as gross misconduct helps employees understand the seriousness of certain actions and their potential career consequences.

Can You Lose Your Final Salary Pension After Being Dismissed?

A final salary pension, also known as a defined benefit pension, is based on the length of service and salary at retirement.

When an employee is dismissed, especially for gross misconduct, concerns naturally arise about how it will impact this type of pension.

Generally, dismissal alone does not wipe out accrued final salary pension benefits. The pension pot built up until the date of dismissal remains intact. However, future benefits stop accruing, and early leaving penalties may apply.

There are rare exceptions, usually in public sector schemes, where pensions can be forfeited if the misconduct causes financial loss or is linked to criminal offences. Understanding scheme-specific rules is key.

How Does Final Salary Pension Differ from Workplace Pension?

A final salary pension, also known as a defined benefit scheme, provides a guaranteed income in retirement based on your final or average salary and years of service. The employer is responsible for funding the promised payout.

In contrast, a workplace pension, often a defined contribution scheme, builds a pension pot through contributions from both employer and employee, plus investment growth. The final value depends on market performance and total contributions.

The key difference lies in who bears the risk, employers for final salary schemes, employees for workplace ones. Leaving the job stops future contributions but doesn’t usually affect already earned benefits.

Does Gross Misconduct Impact Final Salary Benefits?

Gross misconduct can stop future accrual in a final salary pension but doesn’t usually remove the benefits already earned. In rare public sector cases involving criminal acts or financial loss, an employer may seek forfeiture, subject to strict legal approval.

In the private sector, accrued benefits are typically protected, regardless of dismissal reasons. However, leaving employment early may reduce final pension value, especially if salary growth or years of service are cut short. Some schemes also apply early exit penalties.

It’s important to review specific scheme rules and seek legal advice if misconduct involves criminal charges or serious financial implications.

Does Being Sacked Affect Your Workplace Pension Entitlements?

Workplace pensions, also called occupational or defined contribution pensions, work differently. Both the employee and employer make contributions that are invested over time. When an employee is sacked, contributions stop, but the money already paid in remains in the pension pot.

The employee can typically leave the pot where it is, transfer it to another scheme, or consolidate it with other pensions. While dismissal halts future employer contributions, the funds already accumulated remain theirs.

Misconduct does not erase past contributions unless specific forfeiture clauses exist, which is rare in private-sector schemes. It’s essential to contact the pension provider to understand post-dismissal options.

Can An Employer Legally Take Away Your Pension After Dismissal?

An employer cannot usually take away an employee’s pension after dismissal, even for gross misconduct. Pension rights are protected under UK pension laws, and once contributions are made, they are held by the pension scheme, not the employer.

However, in very limited circumstances, especially in public sector pension schemes, an employer can apply for forfeiture if the misconduct caused serious harm, financial loss, or criminal damage.

These applications undergo strict legal scrutiny and must meet high thresholds. For private-sector employees, pension pots are typically unaffected, though stopping future contributions may impact overall retirement savings.

Is Your Occupational Pension Protected Under UK Law?

Occupational pensions in the UK are governed by strict regulations that protect members’ accrued benefits. The Pension Schemes Act ensures that once contributions are made, they belong to the scheme member, even if employment ends abruptly.

Even when an employee is dismissed for gross misconduct, their occupational pension remains safeguarded. The only exceptions involve exceptional cases in public sector schemes where forfeiture provisions apply.

Pension protection laws are designed to give employees security over long-term savings, preventing employers from raiding pension pots as a disciplinary measure. Knowing your scheme rules offers clarity on your rights.

Does Dismissal for Gross Misconduct Impact Your State Pension?

State pensions are calculated based on National Insurance (NI) contributions over your working life, not linked to a specific job or employer. To qualify, you typically need at least 10 qualifying years, with full pension requiring around 35 years.

Being dismissed from a job, even for gross misconduct, does not erase past NI contributions. The only impact is that while unemployed, you may not continue contributing, which could slightly reduce the final pension if unemployment is prolonged.

However, you have the rest of your working life to make up for any gaps. The state pension remains largely unaffected by individual employment situations.

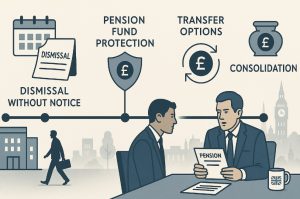

What Are the Pension Rules After Being Fired Without Notice?

Being fired without notice, often called summary dismissal, usually follows gross misconduct and can leave employees wondering what happens to their pension. The reassuring news is that pension rights accrued up to the dismissal date are legally protected.

This means any contributions made by both the employer and employee stay safely invested, and the pension pot remains under the employee’s name.

However, no further contributions are made after dismissal, and any salary-based accruals stop immediately. Employees in public sector schemes should check if forfeiture rules apply, but this is rare and only in severe cases involving criminal acts or public fund losses.

Here’s a summary of how different pensions are affected:

| Pension Type | Effect After Summary Dismissal |

| Defined Contribution | Pension pot preserved; no further contributions from employer/employee |

| Defined Benefit | Accrued service protected; no additional service added after dismissal |

| State Pension | Past NI contributions remain; future accrual depends on employment |

Understanding these rules helps dismissed employees make smart decisions about next steps.

Is There a Forfeiture Clause in UK Pension Schemes?

Forfeiture clauses are rare and mostly appear in public sector schemes. They allow pension benefits to be reduced or reclaimed if an employee’s misconduct results in criminal conviction or public financial loss. Even then, strict legal criteria apply.

What Happens to Contributions After Summary Dismissal?

After a summary dismissal, pension contributions stop immediately, but the money already in the pension pot stays yours.

Both employer and employee contributions made before the dismissal date are protected, and investment growth (or losses) will continue based on market performance. What changes is that no new contributions will be made, and future accrual in final salary schemes ends.

Here’s a quick look at the key points:

| What Stops | What Continues |

| Employee salary-based contributions | Investment growth on existing pot |

| Employer contributions | Ownership of accrued benefits |

| Accrual of future pension service | Right to transfer or consolidate pensions |

Employees should act early by:

- Requesting a final pension statement

- Asking about transfer or consolidation options

- Tracking all old pensions to avoid “lost pots”

Actively managing pensions after dismissal can help minimise long-term retirement impacts and ensure continued financial growth despite the employment setback.

How Can You Protect Your Pension Rights If You’re Facing Dismissal?

Facing dismissal can be stressful, but there are steps you can take to protect your pension rights:

- Understand your scheme rules: Check the terms of your pension to know what’s protected.

- Request a pension statement: Get clarity on accrued benefits and future projections.

- Consult HR or a union representative: They can guide you on your rights.

- Seek independent legal advice: A solicitor can advise on any risks to your pension.

Additional steps:

- Contact your pension provider to understand transfer options

- Keep track of all old pensions

- Consider consolidating small pots for better management

Acting early helps avoid mistakes that could impact your long-term retirement income.

Should You Seek Legal Advice About Pension After Dismissal?

Seeking legal advice is crucial if you are dismissed, especially for gross misconduct. Employment solicitors can explain your pension rights, whether any scheme-specific forfeiture risks apply, and help challenge unfair dismissal if needed.

Legal experts can also help quantify pension losses in cases of unlawful dismissal and guide you through tribunal processes if compensation is warranted.

Even if no wrongdoing is suspected, a legal check ensures you understand how your dismissal impacts your retirement savings. A little advice today can prevent big financial surprises later.

Conclusion

In most cases, being sacked for gross misconduct does not automatically mean losing your pension. Workplace and private pensions remain protected, and only rare public sector situations carry forfeiture risks.

However, dismissal halts future contributions and may affect the size of your retirement pot. Understanding your specific pension scheme, seeking advice when needed, and staying proactive can help safeguard your retirement security even after an employment setback.

Remember, your pension is your long-term financial future, know your rights, take action, and plan wisely.

Frequently Asked Questions

What is the difference between gross misconduct and misconduct in employment law?

Gross misconduct involves serious breaches justifying instant dismissal, while misconduct covers less severe issues usually addressed with warnings.

Are pension contributions affected during a suspension period?

Yes, during suspension, pension contributions typically continue until a final decision is made on dismissal.

How do private pension schemes handle dismissal cases?

Private pension schemes generally protect accrued funds, stopping only future contributions after dismissal.

Can gross misconduct lead to loss of pension benefits in the public sector?

Yes, but only in rare cases where misconduct leads to criminal conviction or financial loss to the public.

Does voluntary resignation protect pension rights?

Yes, voluntary resignation preserves pension rights, with accrued benefits remaining intact.

What role do hr policies play in pension forfeiture?

HR policies outline procedures but cannot override legal pension protections unless specified by scheme rules.

How long does it take to transfer a workplace pension after dismissal?

Pension transfers usually take four to twelve weeks, depending on providers and administrative processes.